Financial Heavy Lifting: Person or Portfolio?

Reading Time: 7 minutes

This is a reminder that your contributions and withdrawal rates are an important, if not the most important aspect of your financial planning success.

It is not the fact that we should not be concerned by investment returns, on the contrary the investment returns are the only meaningful way of providing inflation protection for your finances, it is simply that over short term time periods they cannot be relied upon.

Whereas your contribution rates, and the time that you start those contributions, can be controlled.

To illustrate the importance of your investing timescale and contribution/withdrawal rates below we have set out some examples of their effects.

Contributions

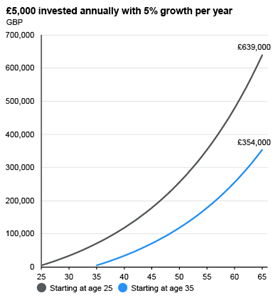

The below chart illustrates an investing rate of £5,000 per annum from the age of 25, with a 5% annual return, to the age of 65.

End portfolio value – £639,000

If that same individual starts investing at 35, using the same assumptions they end up with a portfolio value of £354,000.

To put that another way, to achieve the same portfolio value, with the same level of contributions, they would require the below approximate investment returns per annum:

Age 35 – 8.2% (high but not unheard of)

Age 45 – 15.6% (very unlikely)

Age 55 – 44.7% (a lottery ticket approach)

Source: JPMorgan

Clearly the examples are fictitious as we don’t work with many clients who start their retirement planning at the age of 55!

That being said, the objective of sharing this detail is to confirm the importance of reviewing your savings rate regularly, if not more regularly than your investment returns.

When your investments decline in value what is the real concern, is it that they have fallen to a certain level, or is it in fact that you won’t be able to fund the lifestyle that you want in the future?

A sure-fire way of ensuring that those concerns reduce over time is increasing your contributions at all possible opportunities, rather than relying on investment returns always being higher. If you are already concerned about the investment returns and having a retirement shortfall, would you want to increase your investment returns at that point, and thus potential volatility, or rely on something you can control?

As a side note to our comments relating to contribution rates we must be aware of the concept of Lifestyle Creep affecting our ability to save more in the future.

Definition: Lifestyle Creep

Lifestyle creep occurs when an individual’s standard of living improves as their discretionary income rises and former luxuries become new necessities. The rise in discretionary income can happen either through an increase in income or decrease in costs. The downside of this creep is that when income decreases, for instance with unemployment or in retirement, people will run out of savings as they continue to live above their means. (Source: Investopedia)

Withdrawals

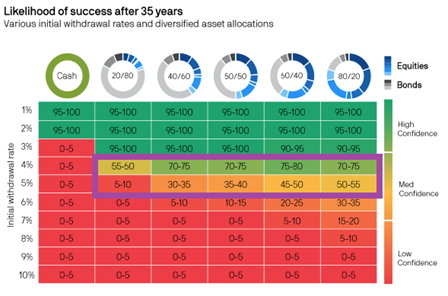

The graphic below illustrates how withdrawal rates, and the make up of your portfolio, also play just as an important role in financial success.

Source:JPMorgan

What is illustrated by the graphic is confidence rating, as a percentage, for various withdrawal rates and portfolio strategies.

At the top left of the table is an example of an account held 100% in cash and being drawn down on at a rate of 1% per annum.

At the bottom right of the table is an example of an account invested 80% in equities and 20% in Bonds and is being spent at a rate of 10% per annum.

We have highlighted the area in purple to show how a small change in the spending level from 4% per annum to 5% per annum could affect the likelihood of achieving success over a retirement period.

As with the contributions example, this is illustrative and by no means a standard client example.

What it does show again is the importance of your part in the success of the financial plan, i.e. your spending, rather than the investment returns.

The key action point and takeaways from this Briefing are twofold.

- The next time the inevitable happens and your investments temporarily decline, first consider your contribution level. The declines are expected and are an opportunity for the regular investor, although they cannot be predicted. The contributions can be changed at any point.

- Within our process, we will always want a detailed breakdown of your expenses. We hope it is clear now why this is so important, in enabling Monenti Partners to work with you to recommend the optimal savings and withdrawal rates that will get you across the financial finish line.

https://www.investopedia.com/terms/l/lifestyle-creep.asp

https://am.jpmorgan.com/gb/en/asset-management/adv/insights/market-insights/guide-to-the-markets/

https://am.jpmorgan.com/us/en/asset-management/adv/insights/retirement-insights/guide-to-retirement/

This Briefing is intended only for clients and prospective clients of our practice. It is designed to inform, educate, and entertain. It does not constitute advice. If you would like a detailed discussion of your financial planning, or any other point raised here, then please do not hesitate to contact us. Please note that past performance is not necessarily a guide to the future and investors may not get back the amount originally invested as the value of any investment and the income from it is not guaranteed. The Financial Conduct Authority do not regulate taxation advice.

The value of investments can go up as well as down, so you could get back less than you invested. This website and its content do not constitute advice, and our services are designed for those resident in the UK.

Monenti Partners Ltd is a company registered in England under number 06299795 Registered office address Castle House, Castle Street, Guilford, GU1 3UW

We are Independent Financial Advisers authorised and regulated by the Financial Conduct Authority (FRN) 485058.