Mr & Mrs Approaching Retirement

Reading Time: 7 minutes

Retirement is a significant milestone in most of our lives. Let us introduce you to ‘Mr. & Mrs. Approaching Retirement’; a couple in their mid-50s who were introduced to Monenti Partners as they prepared to embark on their golden years. In this article, we will delve into their financial planning journey, the questions they had and uncertainties they faced, the steps we took, and ultimately the value they gained from seeking professional advice. Whilst this case study is based on a real-life client scenario, it is only an example and individual advice should be sought in all circumstances.

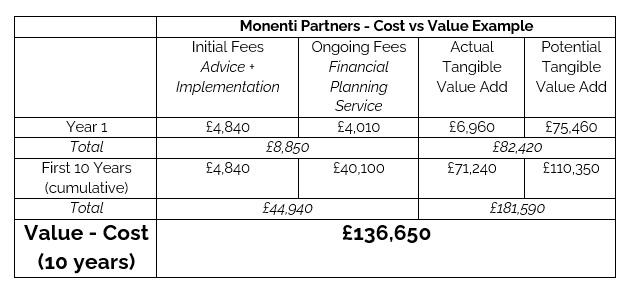

To start at the end, below is the outcome of the initial planning that we undertook both in the first year of engagement and the potential value at the 10-year mark. Please note that the below does not include further advice areas that are recommended for the clients. Should you wish to receive the calculations behind the below then please do get in contact.

Client circumstances and background

‘Mr. & Mrs. Approaching Retirement’ were recommended to Monenti Partners by friends who had already experienced the benefits of our Financial Planning Service. They live in the London area with three children, who are beginning to embark on their own careers. Mr. is a former professional services executive, now working as a teacher, and hoping to retire within the next five years. Mrs. took a career break to raise the children and currently manages the family finances.

Over the years they have accumulated a range of financial assets, most notably their home and an additional residential rental property portfolio, plus other cash savings, investments, and pensions from previous employment.

They are active members of their local community, engaging in sports activities with their children as well as volunteering, and they envision a long and fulfilling retirement together. They had not previously conducted any formal Financial Planning via a regulated adviser.

Financial uncertainties and questions pre-engagement

Prior to engagement ‘Mr. & Mrs. Approaching Retirement’ had several financial uncertainties and questions. These included:

1. Clarifying their retirement plans and understanding the income they would require.

2. Determining if they could afford for Mr. to stop working in the short term and evaluating the income provided by their various pensions, including the Teachers’ Pension.

3. Reviewing the appropriateness of their existing assets and identifying any beneficial changes.

4. Creating a cohesive investment strategy across their portfolio and seeking alternative investment options beyond generic “recommended buy” lists.

5. Simplifying their finances and reducing ongoing decision-making.

6. Assessing their ability to financially support their children, particularly with housing costs.

7. Ensuring their wishes would be carried out in the event of premature death or serious illness. Would the other be adequately provided for in either circumstance?

8. Identifying any risks or opportunities they might have overlooked.

What initial planning process was followed?

To address their concerns and guide them towards a secure retirement, we took ‘Mr. & Mrs. Approaching Retirement’ through the following initial planning process:

- Initial phone consultation: A conversation to understand their needs and priorities and answer any initial questions. Following this, we asked the clients to complete questionnaires detailing their current circumstances and attitudes to investment risk.

- Initial planning meeting: Reviewing their financial situation and setting priorities via their Monenti Life Plan, including a budgeting exercise to determine the current ‘Cost of Lifestyle.’

- Engagement letter: As is customary we followed up by setting out the agreed short, medium, and longer-term objectives, along with details of the service level to be offered by Monenti Partners and an estimate of the initial advice costs for the first stage of planning. Once signed, we began gathering full details of their existing policies and prepared our recommendations to restructure their liquid assets in-line with the agreed Monenti Life Plan.

- Investment principles meeting: Whilst the information gathering process was underway, we held an important standalone meeting to discuss key concepts around investment risk, diversification, asset allocation and financial markets to ‘set the scene’ for the coming investment journey. A process we call ‘Lifeboat Drills’.

- Implementation: Acting on the initial recommendations made, including consolidating accounts, aligning portfolios with risk profiles, and optimising tax efficiency.

- Welcome meeting: Once the initial recommendations had been implemented, a second planning meeting was held to revisit the actions taken and key rationale, answer any outstanding questions, and ensure access was established to key resources, such as the use of the ‘My Monenti’ portal, key team contacts, and platform logins.

What are the key benefits & value of the recommendations we implemented?

Tangible vs Intangible – Tangible benefits are those that can be measured financially, while intangible benefits cannot be quantified directly in economic terms, but still have a very significant impact.

The tangible elements of the work we do with clients is often focused on as the primary driver of value. This is because it can be easily calculated, whereas in the main the intangible can only be defined by the client. However, our experience shows that over time the intangible is where most of the value of the ongoing relationship is derived.

Tangible benefits of initial advice include:

- Consolidation of accounts: Reducing the number of accounts from six to five, all held with a single provider, offering online access.

- Aligned portfolios with risk profiles: Ensuring their investments matched their agreed risk profiles and investment objectives, with ongoing monitoring and rebalancing, as needed.

- Improved tax efficiency: Transferring funds from less tax-efficient accounts to more tax-advantaged accounts, such as ISAs and Personal Pensions.

- Simplified administration: Assisting with administrative tasks, ensuring accounts are set up correctly and managing costs effectively.

- Enhanced death benefit arrangements: Aligning pension assets with their circumstances and preferences.

Intangible benefits: The true value of the recommendations and newly established relationship lies in the intangible benefits experienced by ‘Mr. & Mrs. Approaching Retirement.’ These include:

- Confidence: Knowing they can retire on their own terms and maintain their desired lifestyle.

- Peace of mind: Aligning financial resources with their personal objectives and priorities, giving them a sense of control.

- Understanding: Identifying current and future expenses (broadly their ‘Cost of Lifestyle’) as the primary benchmark for measuring progress.

- Financial freedom: The ability to meet their own needs for life, whilst supporting their children’s endeavours and career choices without significant financial constraints.

- Investment knowledge: Enhanced understanding of investment markets and having realistic expectations for the future, increasing psychological resilience during market volatility.

- Simplification: Fewer providers, accounts, and paperwork, reducing administration and complexity.

- Trusted family adviser: Having a reliable source to address their concerns, reduce stress, and guide decision-making.

- Holistic coordination: A financial adviser who can liaise and collaborate with other key professionals, such as accountants and solicitors.

The value of good advice compounds positively, every small impactful decision can make a large difference when looked at over the course of time. The same can be said for not taking an action or making poor decisions. What we have outlined below is the impact of our initial advice and planning both in the first year and over a 10-year period and does not include additional work and value that will be added in future.

Examples of future planning

The initial planning process serves as a foundation for ongoing value creation. Future planning strategies for ‘Mr. & Mrs. Approaching Retirement’ may include:

• Safeguarding the plan against health events or premature death through insurance.

• Ongoing tax planning to optimise reliefs and allowances and to adapt to changing legislation.

• Assessing the need for action regarding the State Pension, considering Mrs.’ career break.

• Reviewing and realigning their rental property portfolio for simplicity, tax efficiency, and increased yield.

• Implementing inheritance tax planning strategies, such as trusts, business relief (BR), protection, and gifting.

• Involving the children in the planning discussions to introduce them to key concepts and ideas.

By engaging with our financial planning process, ‘Mr. & Mrs. Approaching Retirement’ gained clarity, confidence, and a personalised roadmap for their retirement. The tangible benefits of streamlined accounts, optimising portfolios and tax efficiency were complemented by intangible advantages, including peace of mind, simplification, reduced decision making and trusted advisory support. The value of good advice continues to grow over time, and future planning strategies will further enhance their financial well-being. As they approach their retirement years, ‘Mr. & Mrs. Approaching Retirement’ are well-prepared to enjoy a fulfilling and financially secure future.

Sources:

‘Putting a value on your advice: Quantifying Vanguard Adviser’s Alpha in the UK’ – June 2020

This Briefing is intended only for clients and prospective clients of our practice. It is designed to inform, educate, and entertain. It does not constitute advice. If you would like a detailed discussion of your financial planning, or any other point raised here, then please do not hesitate to contact us. Please note that past performance is not necessarily a guide to the future and investors may not get back the amount originally invested as the value of any investment and the income from it is not guaranteed. The Financial Conduct Authority do not regulate taxation advice. The tax treatment of investments depends on individual circumstances and may be subject to change in the future. The value of your investments can go down as well as up, so you could get back less than you invested. A pension is a long term investment. The fund value may fluctuate and can go down. Your eventual income may depend on the size of fund when accessed, interest rates and legislation.

The value of investments can go up as well as down, so you could get back less than you invested. This website and its content do not constitute advice, and our services are designed for those resident in the UK.

Monenti Partners Ltd is a company registered in England under number 06299795 Registered office address Castle House, Castle Street, Guildford, GU1 3UW

We are Independent Financial Advisers authorised and regulated by the Financial Conduct Authority (FRN) 485058.